As you squirrel away your excess cash in a corporate investment account, you eventually face the question of how to convert your savings into retirement income.

If you are seeking a sustainable, life-long retirement income, look no further than the gold-plated “defined” pension plans enjoyed by lucky civil servants. Your corporation can set up a defined pension plan, called an Individual Pension Plan (IPP), for one or two individuals.

The purpose of the IPP is to provide you with maximum lifetime pension benefits permitted under the Income Tax Act. The retirement ages of the IPP are between 55 and 71 years.

The IPP advantages include:

- a greater contribution than what is available under an RRSP;

- a deduction for interest on funds borrowed to make the contribution;

- actuarial, accounting, and administration fees for IPPs are tax deductible in the company and not considered a taxable employment benefit;

- if the return on your investment becomes insufficient to fund the IPP benefits, you can top up the IPP;

- early retirement can be funded by a lump-sum final and tax-deductible contribution;

- IPP pension income is eligible to be split with a spouse at age 50. RRIF income is not eligible for income splitting until age 65.

- the corporation has 120 days after the year-end to make the contribution

- various options are available to pay out retirement benefits.

The IPP disadvantages include:

- since you require the services of an actuary, administrative expenses for IPPs are higher than for RRSPs;

- you cannot make spousal RRSP contributions;

- new RRSP room is restricted to $600 per year;

- you don’t have the ability to withdraw funds prior to retirement.

An actuary is required to prepare a tri-annual valuation of the IPP. If at any time your IPP runs a deficit, the company must make up the shortfall. On the other hand, if your IPP has a surplus, you must reduce your contributions.

IPP Contribution Example

First year maximum past service contribution advantage is shown in the Table 1.

Table 1.

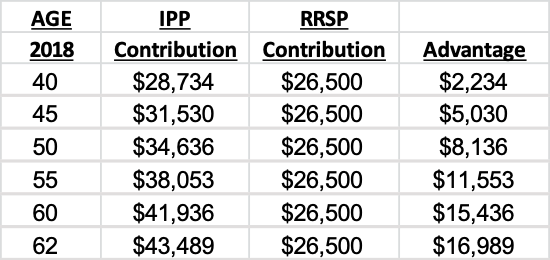

2019 IPP annual contribution advantage is depicted in Table 2.

Table 2.

IPP Benefits

The IPP gives you peace of mind in today’s uncertain investment climate, because you know the amount of retirement pension benefits you will be able to enjoy.

The Individual Pension Plan (IPP) is also a defensive tax strategy to protect your $500,000 Small Business Deduction entitlement, because corporate income put into an IPP no longer generates passive income which could reduce that deduction.